At 1:30 AM, January 12, 2017, the Senate passed a budget resolution to repeal the Affordable Care Act (ACA), with a party-line vote (51-48). A budget resolution needs only a simple majority to pass and thus represented the Republican Party’s quickest avenue to repeal the ACA. Congressional Republicans are pursuing a plan that would repeal parts of the law in early 2017 via budget reconciliation (see below for which parts), but may delay enacting a new system for up to three years (i.e. they plan to defund the ACA’s key coverage provisions, but delay a replacement).

On January 17, 2017, the nonpartisan Congressional Budget Office (CBO) released a report on how ACA repeal would affect health insurance coverage and premiums. The CBO assumed the repeal plan would be similar to that adopted by Congress in 2015 (sponsored by Congressman Tom Price, Donald Trump’s nominee for secretary of Health and Human Services, and vetoed by President Obama). The bill Congress passed did not contain policies intended to replace the ACA, presumably because a consensus did not exist on what form such an alternative should take. It is unlikely that supporters of ACA repeal will have agreed on an alternative before voting on repeal. Based on the 2015 legislation, the CBO report assumes that the forthcoming reconciliation legislation will do the following:

- repeal

- the individual mandate penalties

- after a delay of two years, the premium tax credits and Medicaid expansions

- leave intact the ACA’s insurance reforms (cannot be amended through reconciliation under the Senate’s reconciliation rules)–including

- essential health benefit

- actuarial value requirements

- limitations on health status underwriting

- limitations on pre-existing condition exclusions

- rating requirements that allow premiums to vary only based on age, geographic locations, and tobacco use (and not on sex).

CBO Projections of Impact on Health Insurance Coverage:

If Congress does not repeal the ACA’s insurance reforms (listed above):

- 2017: No immediate dramatic effect because premium increases would already be established and enrollment set

- 2018: 18 million people would become uninsured, including 10 million fewer enrollees in the nongroup (or individual) insurance market, 5 million fewer with Medicaid coverage, and 3 million fewer with employment coverage.

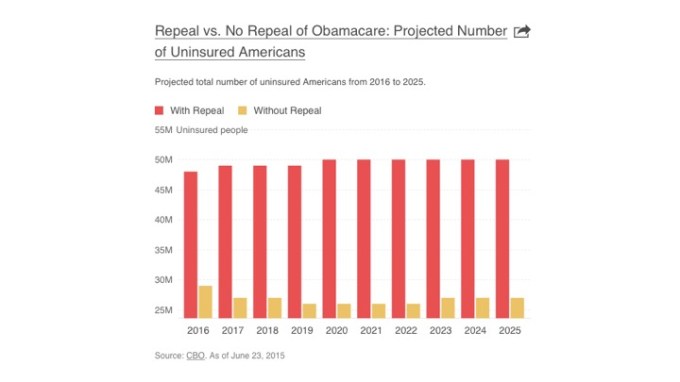

- 2020: (following repeal of the Medicaid expansions and premium tax credits): 27 million will have become uninsured

- 2026: 32 million will have become uninsured (23 million fewer nongroup market enrollees, 19 million fewer covered by Medicaid, and 11 million more enrolled in employer coverage)

- These increases would be due to a combination of people dropping coverage because it was no longer mandated and to insurers abandoning the nongroup market and increasing premiums because of adverse selection concerns.

If Congress does repeal the ACA’s insurance reforms (listed above):

- 2026: 59 million would be uninsured; 21 percent of the population.

CBO Projections of Impact on Health Insurance Coverage:

- 2018: insurers would increase premiums by 20 to 25 percent

- 2018: insurers in some areas would leave the nongroup market in anticipation of further reductions in enrollment and higher average health care costs among enrollees who remained after the subsidies for insurance purchased through the marketplaces were eliminated. As a consequence, roughly 10 percent of the population would be living in an area that had no insurer participating in the nongroup market.

- 2020: nongroup market premiums would increase by 50 percent relative to current law projections and about half of the population would live in states with no insurer participation in the nongroup market

- 2026: nongroup market premiums would double and three-quarters of the population would live in states with no insurers in the nongroup market. Fewer than 2 million people would have nongroup market coverage.

The Urban Institute has released a similar Report on the Implications of Partial Repeal of the ACA through Reconciliatio, in December 2016, using the same 2015 bill as the model for the 2017 reconciliation bill repeal.

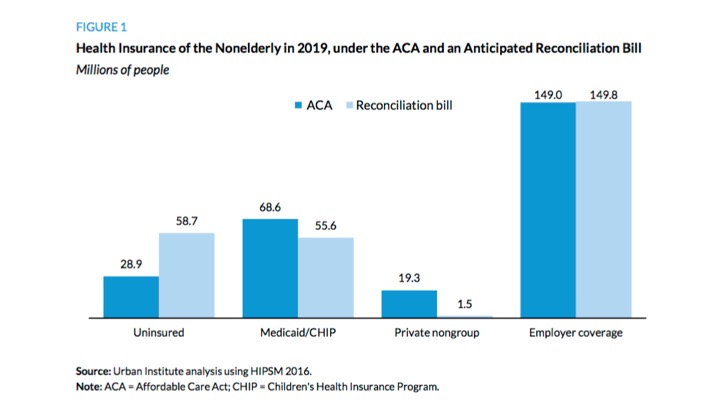

The key effects of the passage of the anticipated reconciliation bill are as follows, quoted verbatim from the report’s Abstract:

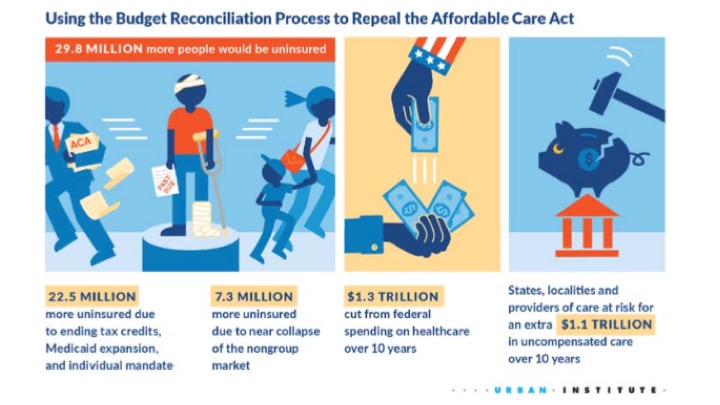

- The number of uninsured people would rise from 28.9 million to 58.7 million in 2019, an increase of 29.8 million people (103 percent). The share of non-elderly people without insurance would increase from 11 percent to 21 percent, a higher rate of uninsurance than before the ACA because of the disruption to the non-group insurance market.

- Of the 29.8 million newly uninsured, 22.5 million people become uninsured as a result of eliminating the premium tax credits, the Medicaid expansion, and the individual mandate. The additional 7.3 million people become uninsured because of the near collapse of the non-group insurance market.

- Eighty-two percent of the people becoming uninsured would be in working families, 38 percent would be aged 18 to 34, and 56 percent would be non-Hispanic whites. Eighty percent of adults becoming uninsured would not have college degrees.

- There would be 12.9 million fewer people with Medicaid or CHIP coverage in 2019.

- Approximately 9.3 million people who would have received tax credits for private non-group health coverage in 2019 would no longer receive assistance.

- Federal government spending on health care for the non-elderly would be reduced by $109 billion in 2019 and by $1.3 trillion from 2019 to 2028 because the Medicaid expansion, premium tax credits, and cost-sharing assistance would be eliminated.

- State spending on Medicaid and CHIP would fall by $76 billion between 2019 and 2028. Also, because of the larger number of uninsured, financial pressures on state and local governments and health care providers (hospitals, physicians, pharmaceutical manufacturers, etc.) would increase dramatically. This financial pressure would result from the newly uninsured seeking an additional $1.1 trillion in uncompensated care between 2019 and 2028.

- The 2016 reconciliation bill did not increase funding for uncompensated care beyond current levels. Unless different action is taken, the approach will place very large increases in demand for uncompensated care on state and local governments and providers. The increase in services sought by the uninsured is unlikely to be fully financed, leading to even greater financial burdens on the uninsured and higher levels of unmet need for health care services.

- If Congress partially repeals the ACA with a reconciliation bill like that vetoed in January 2016 and eliminates the individual and employer mandates immediately, in the midst of an already established plan year, a significant market disruption would occur. Some people would stop paying premiums, and insurers would suffer substantial financial losses (about $3 billion); the number of uninsured would increase right away (by 4.3 million people); at least some insurers would leave the non-group market midyear harming consumers financially.

- Many, if not most, insurers are unlikely to participate in Marketplaces in 2018—even with tax credits and cost-sharing reductions still in place—if the individual mandate is not enforced starting in 2017. A precipitous drop in insurer participation is even more likely if the cost-sharing assistance is discontinued (as related to the House v. Burwell case) or if some additional financial support to the insurers to offset their increased risk is not provided.

The Urban Institute’s report concludes:

This scenario does not just move the country back to the situation before the ACA. It moves the country to a situation with higher uninsurance rates than was the case before the ACA’s reforms. To replace the ACA after reconciliation with new policies designed to increase insurance coverage, the federal government would have to raise new taxes, substantially cut spending, or increase the deficit.

Leave a comment